Carrier vs. Carrier Comparisons

Related Companies

In the midst of a car accident or fender-bender, the initial question that comes to your mind probably won’t be whether you should file an auto insurance claim. However, once the adrenaline and shock have worn off, you will have a big decision to make. Do you file a claim and risk a possible increase to your car insurance rate, or do you pay for the repairs (if any) out of pocket?

If you're trying to figure out "should I file a car insurance claim," here's everything you need to know about when to make a claim and how to decide if you need to.

Save Money by Comparing Insurance Quotes

Compare Free Insurance Quotes Instantly

Secured with SHA-256 Encryption

When to Make an Auto Insurance Claim

The circumstances behind an auto accident can be unique, but typically, you'll want to make an auto insurance claim in these situations.

You're Dealing With Another Driver

Anytime your accident involves another driver, you'll almost always want to file an insurance claim. This includes cases where there are no injuries or only minimal damage to the vehicles.

Assume you're in a fender-bender that doesn't cause an injury, but the other person has a couple of dents in their car. Rather than deal with insurance policies, the other driver says they'll send you a bill for the repairs, and you can pay out of pocket.

In that situation, paying for the repairs yourself may seem like the more straightforward move, but it's also risky. Even if they send you a bill for the repairs, the driver could come back months later, claiming that there was more damage. Or perhaps, they could even try inflating the cost of the repairs to get more money from you.

Unfortunately, when you're dealing with a stranger, it's impossible to know what their intentions are. If you have liability insurance, which most states require by law, your insurance company can protect you from lawsuits. They may even pay for any legal defense fees you may have. Not to mention, insurance companies are well-equipped to handle angry drivers, regardless of how upset they might be.

The same logic applies when you're dealing with your own car wreckage. The other driver may promise that they'll pay for your vehicle's damage, but once they see the bill, they might change their mind.

There's Serious Damage to You or Someone Else's Vehicle

Even if the damage looks minor and the other driver is honest, it can be tricky to judge repair costs by appearance. What may look like a harmless dent or a couple of scrapes could end up being thousands of dollars worth of damage. If you've got liability damage, there's no reason to take that gamble.

Your car could also have hidden damage or could end up a total loss. As long as you've got collision insurance, your insurance company will help pay for any repairs you need, minus the deductible. Of course, if you want your insurance company to pay, you'll need to file the claim within a reasonable amount of time.

You're much more likely to get a payout if you make a claim a couple of days after the accident versus a couple of months later.

You or Someone Else Has an Injury

There may not be any damage to the vehicles, but that doesn't mean you or the other driver got away scot-free. It's not uncommon for there to be an injury after a collision, even if the accident itself seems minor. Of the six million accidents that occur annually, nearly three million drivers deal with injuries afterward, and two million suffer permanent injuries.

Unfortunately, like hidden damage, it's not always easy to tell the extent of your own or someone else's injury by appearance. For instance, whiplash can have a delayed onset, and you may not feel it for up to twenty-four hours after the initial collision.

Some internal injuries, such as broken ribs or internal bleeding, may not be obvious at first with all the adrenaline coursing through your system, but they can become apparent later on. For this reason, many medical professionals urge people to go to the emergency room or urgent care after an accident if they're feeling any pain at all.

Even if the other driver promises that they feel fine and there's no reason to file a claim, they could change their mind later. You don't want to be on the hook for thousands of dollars worth of medical bills.

Save Money by Comparing Insurance Quotes

Compare Free Insurance Quotes Instantly

Secured with SHA-256 Encryption

When You May Not Need to Make an Auto Insurance Claim

While there are plenty of circumstances that warrant filing an auto insurance claim - usually when it involves injuries, vehicle damage, or other drivers - there are a few times when you may not need to bother making a call to your insurance company.

There's Minimal Damage (And You're the Only Person Involved)

If you're the sole person involved and you can tell there's minimal damage, it might not be worth filing a claim. For example, let's say you back into your mailbox while pulling out of the driveway. Nobody else got hurt, and the only visible damage you can see is a few dents and scrapes to your bumper.

In this case, making the call might be unnecessary, and the insurance payout you receive may not be worth risking an increased insurance rate. Additionally, if you don't have collision insurance, your insurance company won't cover your vehicle’s damage anyway.

If you do have collision insurance but think the damage might be worth less than your deductible, you can always get a quick repair estimate. If it's as minor as it seems, there's no reason to file. However, if there's hidden damage lurking beneath the surface, you can always change your mind and make a claim.

Keep in mind that most policies include a deductible that's around $500 or more, and if the repairs aren't more than that, your insurance company won't pay either way.

If Making a Claim Could Raise Your Rates

If the damage is worth more than your deductible and you've got collision insurance, you've got a decision to make: either file a claim and risk increased rates later on or pay out of pocket.

Your insurance rates won't always spike after an accident, and it can depend on your claims history as well as other regulations your insurance company may have for adding surcharges. A surcharge, which is the official term for pay spikes to your premium, can sometimes last for years and gradually decrease for each subsequent year you don't have an accident.

Since the rules regarding surcharges can vary from company to company, the only way to know for sure is to talk to an agent about their surcharge schedule. You don't have to disclose that you were in a collision, but the agent will most likely make a note that you asked about it.

Ultimately, if there's nobody else involved, the damage is minimal, and you can afford to pay out of pocket for the repairs, you may not need to file a claim.

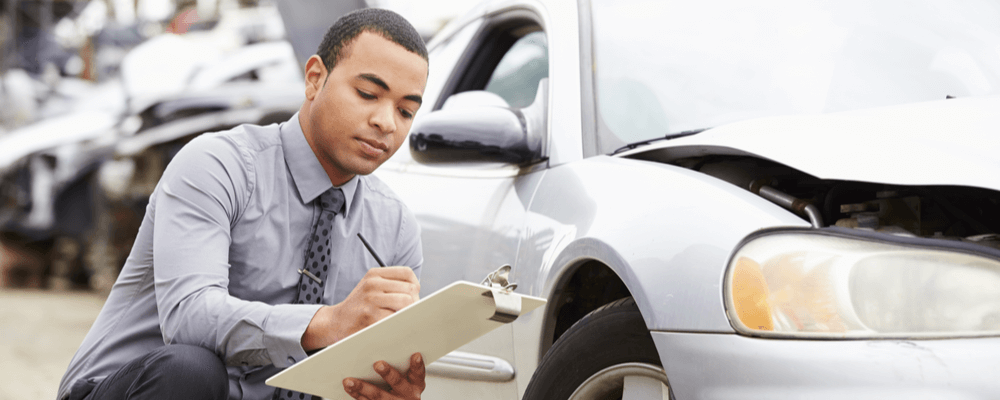

How to Prepare for an Auto Insurance Claim

Let's pretend you've already answered yes to the question of "Should I file a car insurance claim?" At this point, you'll need to begin preparing to make your claim - the sooner, the better.

Preparing for a claim often starts at the scene of an accident. If the collision is with another driver, you'll want to call the police immediately to report the incident, give the driver your insurance information, and let your insurance company know as soon as possible. Depending on the severity of the accident, police officers may not actually come to the scene - especially if there are no injuries and only minor property damage.

In this case, you can always follow up by filing a report at the police station. Most of the time, insurance companies will require that you at least have a police report on file if you plan to make a claim.

If you can, it's always a good idea to take a few photos of each car. The more evidence you have for your claim, the smoother the process is likely to go.

Once you talk to an agent, they'll be able to let you know all the documentation you need as well as an estimate of when you're likely to see a payout. There may also be a few more critical questions you need to ask about your policy, such as:

- Is there a deadline for submitting bills or filing a claim after an accident?

- What's the timeline for handling claim disputes?

- When can you expect the insurance company to contact you? (Most agents will follow up shortly to ask you more questions about the incident or call to let you know if they need additional paperwork).

- If your car will be in the shop for multiple days with repairs, does your policy pay for a rental car?

Even if the accident is minor and you don't plan on making a claim, it's still a good idea to keep any documentation about the accident or any bills you receive from a mechanic.

Save Money by Comparing Insurance Quotes

Compare Free Insurance Quotes Instantly

Secured with SHA-256 Encryption

Image source: Monkey Business Images/ shutterstock.com