Carrier vs. Carrier Comparisons

Related Companies

Buying a new car is exciting, but totaling it can be a nightmare — especially if you owe more than the car’s worth. Since your loan doesn’t disappear, you may have to pay the difference if your insurance payout falls short. Gap insurance protects against this, making it a smart add-on to comprehensive car insurance for new car owners.

However, is gap insurance a yes or no for you? It depends on your loan and car value. Metromile offers the cheapest gap insurance at $67 a month. Learn more about gap insurance, then compare rates to find affordable coverage. Enter your ZIP code to get personalized insurance quotes tailored to your needs and budget.

What You Should Know

- Gap insurance stops loan payments on a totaled car

- Insurers offer cheaper gap coverage than dealerships

- You can cancel gap insurance once your loan decreases

Understanding Gap Insurance

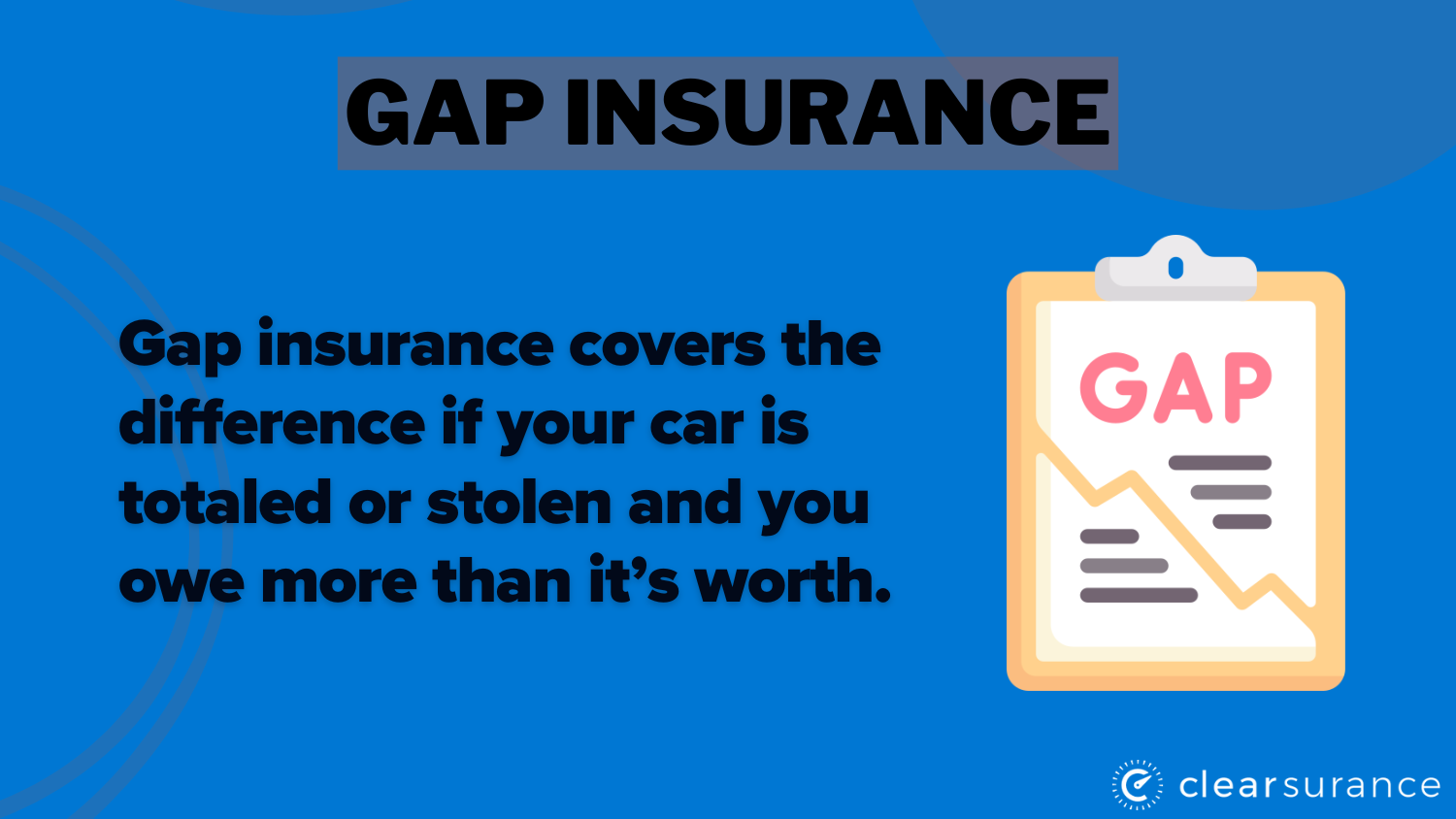

Gap stands for Guaranteed Asset Protection and is an add-on that pays off the remainder of a loan or lease if you total your car. It also covers your vehicle if someone steals it and it isn’t recovered.

Unless you paid a large down payment, you’ll likely owe more on a loan or lease than your vehicle is worth for the first few years. When you owe more on your loan than your car is worth, your loan is considered upside-down or underwater.

While an upside-down loan isn’t usually a problem, it becomes an issue if you total your car. Comprehensive and collision insurance will pay for a totaled car, but your insurance company will only cover your vehicle’s actual cash value (ACV).

Read More: Collision vs. Comprehensive Coverage: Differences in Car Insurance Policies

If your car’s ACV is lower than what you owe on the loan, you’ll be stuck paying for a vehicle you no longer own. Gap insurance protects you from falling into this situation — it pays off the remainder of your loan. This explains the meaning of gap insurance and how it protects you financially.

How Gap Insurance Works

With the exception of a few classic or collectible cars, vehicles lose value with every passing year. Depreciation is essentially what gap insurance protects against. Gap car insurance protects against vehicle depreciation, covering the difference between your car’s actual cash value (ACV) and the remaining loan balance if your car is totaled.

For example, if your car’s ACV is $10,000 but you owe $15,000, gap insurance covers the $5,000 gap. Only new cars qualify, and you must have collision and comprehensive coverage. While helpful, there are cases when gap insurance does not pay — like if you miss loan payments or your car's value exceeds the loan.

If you're wondering, "Do I need gap insurance if I have full coverage?" Full coverage won’t cover loan gaps, so gap insurance may still be necessary. Speak with an insurance representative to check eligibility, as requirements vary.

Gap Insurance: Where to Buy and Monthly Cost

There are two main options for where to buy gap insurance — from an insurance company or a car dealership. Not all insurers offer it, so you may need to shop around to find who offers gap insurance.

You can buy gap insurance through a dealership, usually at a higher cost, but they can roll it into your car loan or lease, adding it to your monthly payment. Insurance companies are usually the cheapest option for gap insurance. Geico's gap insurance can be added to your policy, often by speaking with a representative or sometimes online.

Transportation is one of the biggest expenses for most households. Fortunately, car insurance doesn't have to cost too much. Check out 6 ways you could lower your bill, including discounts https://t.co/1Vc8uwPGr2 pic.twitter.com/3z4NF8TIzN

— Metromile (@Metromile) October 1, 2020

If you're wondering, "How much is gap insurance per month?",it typically ranges from $67 to $95 monthly, depending on the car make and model and the loan amount. See the table below and compare monthly rates from top providers:

| Insurance Company | Monthly Rates |

|---|---|

| $72 | |

| $90 | |

| $82 | |

| $78 | |

| $67 | |

| $95 | |

| $75 | |

| $80 | |

| $86 | |

| $88 |

To find the best gap insurance companies, compare rates and coverage options carefully. Whether you choose gap insurance from a dealer or insurance company, reviewing monthly rates ensures you get the best deal for your coverage needs.

Depreciation Affects Gap Insurance Costs

The rate of your car’s depreciation affects how long you need gap insurance. Cars that depreciate slowly require coverage for a shorter time since you pay off your loan faster than the car loses value.

Vehicles like Jeep Wranglers, which hold their value well due to steady demand, often need less gap coverage. Some of the slowest depreciating cars include the following models:

- Chevrolet Corvette

- Dodge Challenger

- GMC Sierra

- Porsche 911

- Tesla Model X

On the other end of the spectrum, some cars have a reputation for losing value quicker than others. Vehicles with the fastest rates of depreciation include the following models.

- Audi A6

- Acura RLX

- BMW 5 and 7 Series

- Mercedes-Benz S and E-Class

- Volvo S60

Luxury cars often lose value quickly since buyers rarely purchase them for use. Regardless of depreciation, gap insurance can save you thousands if your car is totaled. To avoid overpaying, monitor your car’s ACV against your loan balance and cancel gap coverage once you pay down the loan. Explore ways to get cheap car insurance to further reduce costs.

Totaled Car Insurance State Laws & Thresholds

Laws vary by state, but most companies consider a car totaled when the cost to repair it is higher than the car’s ACV. Each company is different, but most companies will declare a car totaled when the cost to repair is 75% to 90% of the vehicle’s ACV. Your car will also be declared totaled if it’s stolen and can't be recovered.

Most states use a formula to determine the total loss threshold that local insurance companies must adhere to, which can vary by vehicle and the cost of the claim. However, the 22 states listed below set a specific threshold all vehicles must meet. Check your state's laws below to get a better idea of when your car might be declared a total loss.

| State | Total-Loss Threshold |

|---|---|

| Alabama | 75% |

| Arkansas | 70% |

| Colorado | 100% |

| Florida | 80% |

| Indiana | 70% |

| Iowa | 50% |

| Kansas | 75% |

| Kentucky | 75% |

| Louisiana | 75% |

| Maryland | 75% |

| Michigan | 75% |

| Minnesota | 70% |

| Missouri | 80% |

| Nebraska | 75% |

| Nevada | 65% |

| New Hampshire | 75% |

| New York | 75% |

| North Carolina | 75% |

| North Dakota | 75% |

| Oklahoma | 60% |

| Oregon | 80% |

| South Carolina | 75% |

| Tennessee | 75% |

| Texas | 100% |

| Virginia | 75% |

| West Virginia | 75% |

| Wisconsin | 70% |

| Wyoming | 75% |

When your car is declared a total loss, your insurance company usually keeps the vehicle and sells it for salvage. The check you’ll receive for your car depends on the coverage in your policy.

Read More: Tips to Negotiate the Best Settlement for My Totaled Car

Pros and Cons of Gap Insurance

Gap auto insurance offers valuable protection for your car, but it's not recommended for everyone. Like all other types of insurance, gap coverage has pros and cons. First, consider the pros:

- Pays off an upside-down loan if you total your car

- You only have to pay for it as long as you need it — once you pay down your loan, you can cancel it

- Gap insurance is usually a cheap addition to your policy

Although gap insurance can save you a lot of money, it’s not the best choice for every driver. Here are a few cons to look out for:

- Only new cars are eligible for coverage

- Gap insurance is only useful for a short time

- Other options might have better coverage for your needs

The best gap insurance is ideal for new car owners with a loan or lease, but it’s important to explore your options. Be sure to check the best gap insurance reviews and understand how the claim process works to find the right coverage for your situation.

Read More: When to File a Car Insurance Claim

Gap Insurance Discounts & Coverage

Gap insurance provides essential protection for those with a car loan or lease by covering the difference between your car’s actual cash value (ACV) and the remaining loan or lease balance if your car is totaled or stolen.

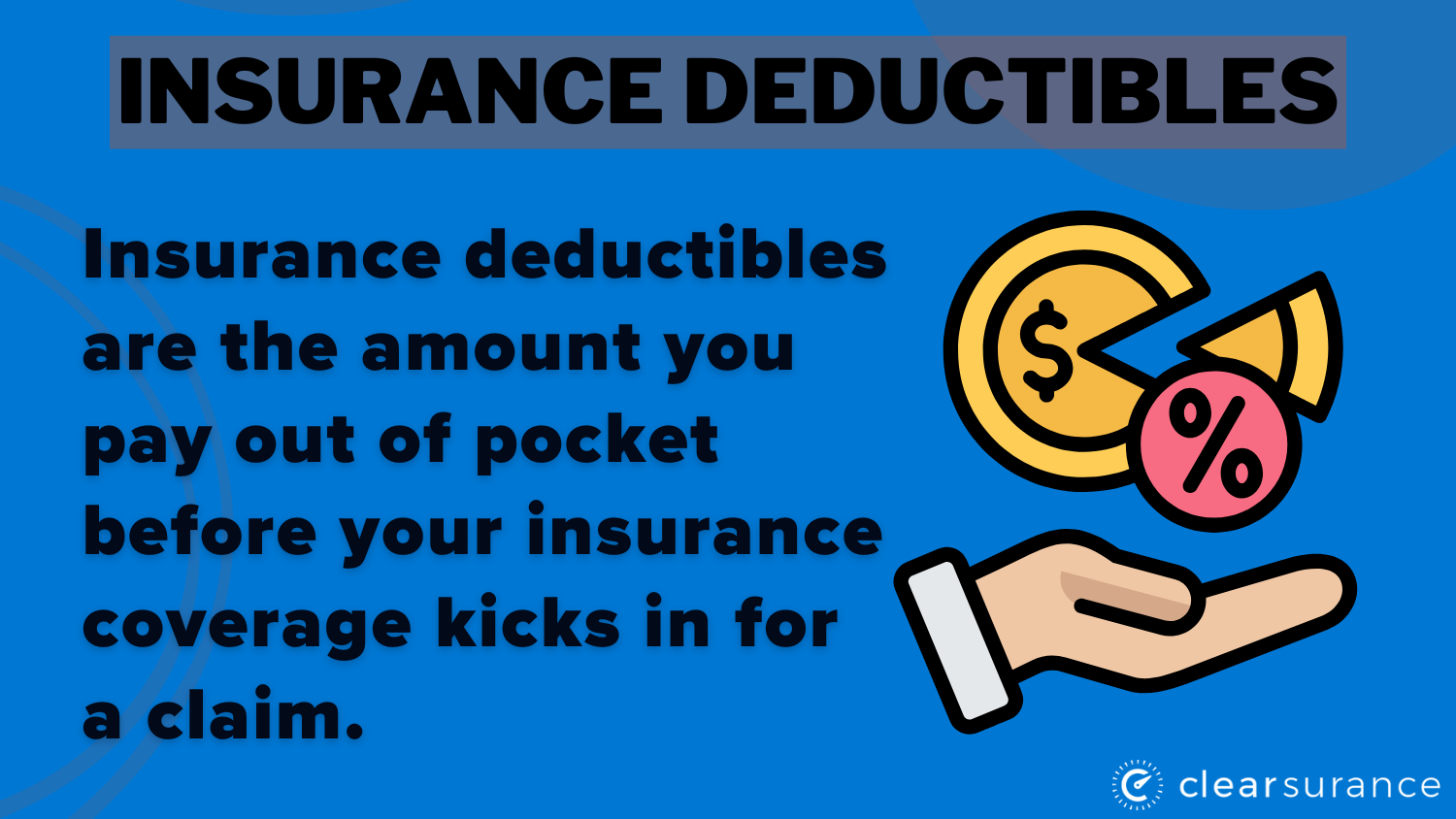

It helps with negative equity but doesn’t cover insurance deductibles, late fees, mileage penalties, security deposits, extended warranties, down payments, or carry-over balances from previous loans.

While gap insurance doesn’t cover every expense, it can prevent out-of-pocket costs for an upside-down loan, making it a valuable option depending on your financial situation. In addition to financial protection, having gap insurance might qualify you for certain car insurance discounts.

| Insurance Company | Available Discounts |

|---|---|

| Safe Driving Discounts; Personalized Rates Based on Mileage and Driving Habits | |

| Discounts for Low-Mileage Drivers and Safe Driving Behavior | |

| Usage-Based Discounts for Good Driving Habits | |

| Lower Rates for Low-Mileage Drivers; Potential Additional Savings for Good Driving | |

| Discounts for Multi-Vehicle Policies and Safe Driving History | |

| Competitive Pricing for Drivers With Low Annual Mileage | |

| 10% Participation Discount on Signup; Up to 40% Off at Renewal for Safe Driving | |

| Personalized Discounts Based on Real-Time Driving Data | |

| Potential Savings for Careful Driving and Low Mileage | |

| Discounts for Military Members and Low-Mileage Drivers |

Many companies offer savings for safe driving, low mileage, or participation in usage-based programs. For example, Nationwide offers up to 40% off for safe drivers, while Progressive and State Farm provide personalized discounts based on real-time driving data. Exploring your insurer’s discounts can lower premiums while keeping gap coverage.

How to Check if You Have Gap Insurance

To check if you have gap insurance, start by reviewing your car insurance policy—most insurers let you view coverage details online or through a representative. If it’s not listed, check your car loan or lease agreement, either by reading the contract or contacting your dealership.

Don’t assume gap insurance is automatically included—it’s not always part of a loan or lease. If you're considering adding it, act quickly, as most insurance companies won’t sell gap coverage after you’ve owned your car for 30 days.

Read More: Best Car Insurance for Leased Vehicles

Alternatives to Gap Insurance

Gap coverage doesn’t fit every driver’s needs, even if you qualify for it. However, gap insurance isn’t your only option for protection when you have a loan or lease. Consider the following alternatives to gap insurance:

- Loan-Lease Insurance: Loan-lease coverage is popular because it works similarly to gap insurance but covers more cars. You can also buy loan-lease insurance whenever you need it instead of in the first 30 days of your ownership.

- Replacement Value Coverage: If you opt for this coverage, your insurance company will pay to replace your new car with a similar make and model rather than cover its ACV.

- Better Car Replacement Insurance: A few insurance companies offer an add-on that will replace a totaled car with a newer model, though it can significantly increase your rates.

Choosing the right option depends on how much you want to spend when you buy your car and what your car insurance company offers. If you can’t decide which option would work best for you, an insurance representative can provide more guidance.

Gap Insurance: When It's Worth It

Gap insurance is ideal for those who leased a car, took a loan of 60 months or more, bought a fast-depreciating vehicle, or made a down payment of less than 20%. It helps cover the gap between your car's value and loan balance if your car is totaled. Below is a Reddit review from a car owner explaining why gap insurance is worth it:

Comment

byu/Robocat110 from discussion

inaskcarsales

This gap insurance Reddit review shows how skipping this insurance led to unexpected debt after a total loss. Most users find it valuable when financing new vehicles with minimal down payments. However, it may not be worth it if you make a large down payment, choose a short-term loan, or buy a used car.

Gap coverage also doesn't benefit those who own their car outright. Consider your loan terms and car value to decide if gap insurance fits your needs.

Read More: Best Car Insurance Companies That Cover Any Car You Drive

Find the Best Gap Coverage for Your Car

Understanding gap insurance provides crucial financial protection for drivers with new cars or significant loans. The best gap insurance shields you from potentially devastating debt if your vehicle is totaled while underwater on your loan.

Among gap insurance companies, Metromile offers the most affordable rates at $67 monthly, making it the best place for budget-conscious drivers to get gap insurance.

Whether purchased through dealerships or the best car insurance companies, this coverage delivers peace of mind, knowing you won't face thousands in loan payments for a car you no longer own.

Evaluate your financial situation carefully to determine if this valuable protection aligns with your specific needs. You can also enter your ZIP code into our free comparison tool to start comparing rates now.

Frequently Asked Questions

What does gap insurance mean?

Gap stands for Guaranteed Asset Protection, and it protects you from paying for a car loan on a vehicle you no longer own.

Do you need gap insurance after you buy a car?

Some car loan lenders and leasers require you to carry gap coverage, but it’s not always necessary. You can skip gap insurance if you put more than 20% down when you buy the car, or your loan will be less than 60 months long.

Read More: How soon do you need insurance after buying a used car?

What does gap insurance do?

If you total a car you don’t own outright, you might owe more on your loan than the vehicle is worth. Gap insurance pays the difference between what you owe and what your car is worth.

Can you buy gap insurance at any time?

Most gap insurance add-ons must be purchased within 30 days of buying a car, and you usually have to be the first owner to qualify. If that doesn’t apply to you, loan-lease insurance might work.

How do you get gap coverage?

You can purchase gap coverage by asking your insurance company to add it to your policy. Best gap insurance companies offer various options to protect you from financial loss. Alternatively, you might be able to add gap insurance to your car loan or lease at the dealership.

Do you need gap insurance?

Most drivers don’t need gap coverage. The only time you might need gap insurance is when your car’s value is less than what you owe on your loan. Start comparing affordable insurance options by entering your ZIP code into our free quote comparison tool today.

When can you drop gap insurance?

Typically speaking, you can drop gap insurance whenever you’d like. However, you should check with your car loan or lease — some contracts specify how long you need to carry gap insurance.

How do you know if you have gap insurance?

There are two places to check for gap coverage. You can check with your dealership to see if your loan or lease automatically included it. Alternatively, you can look at your car insurance policy to see if you already have it.

Are gap insurance and full coverage the same?

Full coverage car insurance refers to a suite of auto insurance products, including liability, collision, comprehensive, uninsured/underinsured motorist, and medical payments or personal injury protection.

Gap insurance is an add-on that requires at least collision and comprehensive policies and is not the same as full coverage.

Do you get money back from gap insurance?

You won’t get a refund for gap insurance after you cancel it unless you’ve paid for your entire policy upfront and didn’t use all of it. If you have gap coverage included in your loan and you pay your loan off early, you might receive a refund for the unused portion.

Does gap insurance cover theft?

Gap insurance does not cover your car after theft — that’s what comprehensive insurance is for. However, it will cover the difference on your loan if your company declares your vehicle a total loss after a theft.

No matter how much coverage you need, you can find the lowest rates by entering your ZIP code into our free comparison tool.

How long does gap insurance last?

The length of time your gap insurance lasts depends on where you get it from. Gap coverage from a car insurance policy can be canceled whenever you’d like, though the best time is to wait until you pay your loan down. Getting your gap coverage from a dealership will likely last your whole loan or lease.