Best and Cheapest Homeowners Insurance in North Carolina for 2025 (Top 10 Low-Cost Companies)

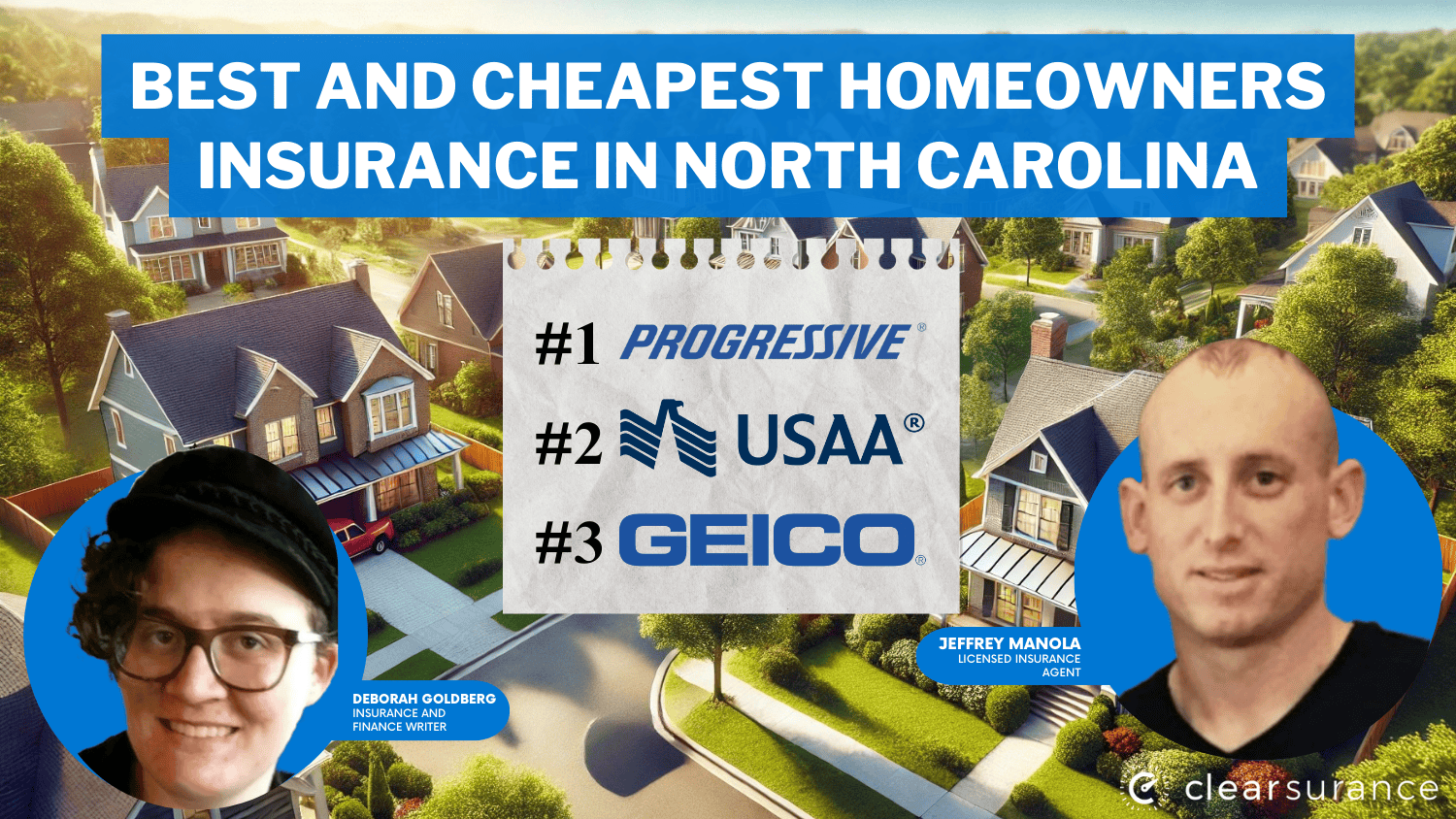

The best and cheapest homeowners insurance in North Carolina from are Progressive, USAA, and Geico, with rates starting as low as $43 a month. Recent North Carolina homeowners' insurance rate increase trends have made shopping for coverage more important than ever.

Coverage varies by provider, and add-ons like flood insurance may be necessary. This guide explores top insurers and ways customers say they’ve saved on homeowners insurance through discounts and customizations, helping you balance affordability and protection for your home.

| Company | Rank | Monthly Rates | A.M. Best | Best For | Jump to Pros/Cons |

|---|---|---|---|---|---|

| #1 | $43 | A+ | Competitive Rates | Progressive | |

| #2 | $$63 | A++ | Military Focus | USAA | |

| #3 | $64 | A++ | Broad Discounts | Geico | |

| #4 | $72 | B | Nationwide Coverage | State Farm | |

| #5 | $75 | A | Customer Satisfaction | American Family | |

| #6 | $88 | A | Flexible Options | Liberty Mutual | |

| #7 | $92 | A | Customizable Policies | Farmers | |

| #8 | $93 | A++ | Long-Term Stability | Travelers | |

| #9 | $107 | A+ | Superior Service | Nationwide | |

| #10 | $113 | A+ | Technology Integration | Allstate |

From Progressive’s $43 monthly rates to Allstate’s tech-driven features, comparing options helps balance coverage and affordability while ensuring the best protection for your home. Make sure to compare home insurance rates by entering your ZIP code to avoid overpaying.

What You Should Know

- 95% of American Family policyholders in North Carolina renew their policies

- Progressive offers $43 monthly rates for $200k coverage

- USAA provides 25% bundling discounts for military families

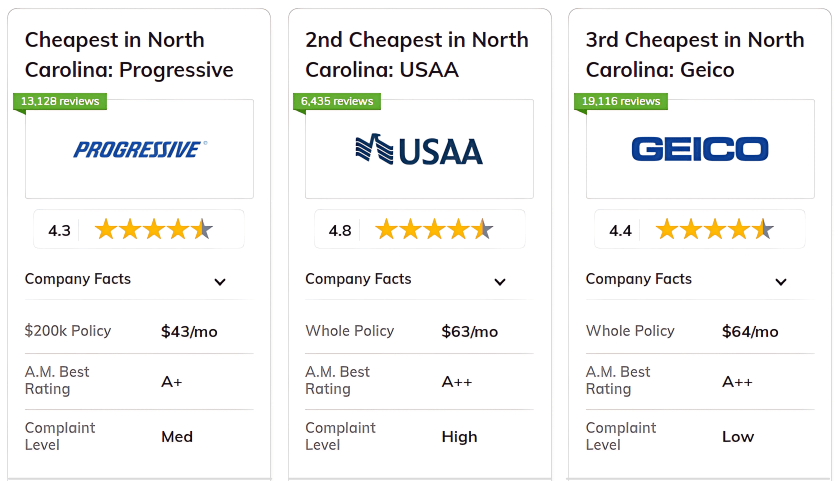

#1 – Progressive: Top Overall Pick

Pros

- Affordable Premiums: Homeowners seeking coverage in North Carolina can access Progressive's $200k policies with monthly payments starting at $43 a month.

- Multi-Policy Benefits: Combining auto and home insurance through Progressive delivers North Carolina residents annual savings averaging $780 on total premiums.

- Digital Experience: Progressive Review indicates their mobile app helps North Carolina homeowners file claims within 15 minutes with instant updates.

Cons

- Limited Local Agents: Only eight certified Progressive insurance agents currently serve homeowners across major cities in North Carolina.

- Coverage Limitations: Homes located 50 miles from North Carolina's coast have substantially higher Progressive insurance deductibles for hurricane coverage.

#2 – USAA: Best for Military Focus

Pros

- Military Expertise: Active service members stationed at Fort Bragg in North Carolina receive specialized deployment protection with zero policy lapses.

- Superior Discounts: USAA review confirms military families save 25% more than other insurers when protecting North Carolina homes.

- Claims Satisfaction: Dedicated military claims specialists process North Carolina homeowner requests within 48 hours through USAA's priority system.

Cons

- Membership Requirements: Strict verification of military service records limits USAA coverage access for many North Carolina homeowners.

- Limited Offices: USAA maintains only two physical service centers in North Carolina, requiring most members to use online services.

#3 – Geico: Best for Broad Discounts

Pros

- Discount Variety: Homeowners installing smart security systems in North Carolina properties receive exclusive 15% premium reductions through Geico partners.

- Competitive Rates: Geico review shows new North Carolina homes under five years old qualify for automatic 8% premium discounts.

- Security Incentives: Impact-resistant roofing materials on North Carolina homes earn property owners up to 10% off their annual Geico premiums.

Cons

- Third-Party Coverage: Unlike direct insurers, Geico's North Carolina policies require approval from multiple underwriting partners before activation.

- Service Limitations: Claim processing for North Carolina Geico policyholders typically takes 72 hours longer than industry standard response times.

#4 – State Farm: Best for Nationwide Coverage

Pros

- Local Presence: State Farm insurance review highlights their network of 350 dedicated agents serving homeowners across all North Carolina counties.

- Claims Processing: Professional adjusters reach damaged North Carolina properties within 24 hours through State Farm's emergency response program.

- Policy Flexibility: State Farm homeowners insurance in North Carolina offers customizable $300k policies starting at $106 monthly with optional coverage add-ons.

Cons

- Premium Increases: First-time North Carolina homeowners face automatic 15% rate increases after filing two claims within three years.

- Coverage Gaps: State Farm home insurance’s basic North Carolina policies exclude essential protections for foundation damage and water backup issues.

#5 – American Family: Best for Customer Satisfaction

Pros

- Satisfaction Rating: American Family review reveals 95% of North Carolina policyholders renew coverage due to exceptional claim experiences.

- Personal Service: Dedicated agents conduct annual policy reviews for North Carolina homeowners to optimize coverage and identify savings opportunities.

- Claims Support: Emergency response teams reach storm-damaged North Carolina properties within 12 hours through American Family's priority system.

Cons

- Coverage Area: American Family's services currently exclude homeowners in 15 rural North Carolina counties.

- Premium Structure: Recent North Carolina residents face higher initial premiums until establishing three years of claims-free history.

#6 – Liberty Mutual: Best for Flexible Options

Pros

- Customizable Coverage: Liberty Mutual shows North Carolina homeowners can adjust deductibles between $500-$5000 for premium savings.

- Payment Options: Flexible monthly payment plans allow North Carolina residents to choose from six different premium scheduling options.

- Emergency Services: Liberty Mutual's preferred contractors reach North Carolina homes within 6 hours for emergency water damage repairs.

Cons

- Rate Stability: New Liberty Mutual policyholders in North Carolina experience premium increases of up to 18% after first-year promotional rates.

- Service Network: Emergency repair services are limited to only 23 certified contractors across North Carolina's major metropolitan areas.

#7 – Farmers: Best for Customizable Policies

Pros

- Policy Customization: Farmers review demonstrates that North Carolina homeowners can select from 15 different coverage enhancement options.

- Renovation Protection: Unique coverage extends to North Carolina homes undergoing major renovations without premium increases during construction.

- Claims Guarantee: Farmers promise North Carolina residents claim decisions within 48 hours, or they waive the deductible.

Cons

- Price Structure: Monthly premiums for North Carolina coastal properties start significantly higher at $168 per month for basic $300k coverage.

- Coverage Limitations: Farmers restrict certain coverage options for North Carolina homes older than 50 years without recent updates.

#8 – Travelers: Best for Long-Term Stability

Pros

- Long-term Savings: Travelers review confirms North Carolina homeowners receive 2% annual premium reductions for claims-free policy maintenance.

- Green Coverage: Eco-friendly home improvements in North Carolina properties qualify for exclusive premium discounts of up to 12%.

- Heritage Protection: Specialized coverage protects historical North Carolina homes while maintaining original architectural features.

Cons

- Initial Costs: New North Carolina policyholders must pay the first three months of premiums upfront before monthly payment options.

- Qualification Process: Travelers require extensive home inspections for North Carolina properties before approving coverage applications.

#9 – Nationwide: Best for Superior Service

Pros

- Service Quality: Nationwide review indicates their North Carolina claims adjusters complete assessments within 24 hours of filing.

- Coverage Options: Premium policies include flood protection for North Carolina homes without requiring separate FEMA insurance coverage.

- Member Benefits: Loyal North Carolina customers receive complimentary annual home maintenance inspections after three years of coverage.

Cons

- Cost Structure: Nationwide requires North Carolina homeowners to maintain a minimum of $500 deductibles regardless of claim history.

- Availability Restrictions: Some premium coverage options remain unavailable for North Carolina homes in hurricane-prone coastal regions.

#10 – Allstate: Best for Technology Integration

Pros

- Digital Tools: Allstate review highlights advanced drone assessment technology for North Carolina roof damage claims within hours.

- Smart Home Benefits: Installing Allstate-approved smart devices in North Carolina homes provides automatic monthly premium reductions.

- Virtual Support: Real-time video assessments allow North Carolina homeowners to file claims instantly through Allstate's mobile platform.

Cons

- Premium Rates: Technology integration fees increase base premiums for North Carolina homeowners by approximately $15 monthly.

- System Requirements: Smart home discounts require North Carolina residents to maintain constant internet connectivity for monitoring systems.

North Carolina Home Insurance Costs by Coverage Level

The average cost of homeowners insurance in North Carolina varies significantly by provider and coverage level, with Progressive offering the lowest rates, starting at $43 a month for a $200k policy, while Allstate has the highest, reaching $231 monthly for a $500k policy.

As property values increase, do you need to increase your homeowners insurance coverage? The table suggests that higher coverage comes at a steep price, as seen with Farmers and Nationwide, whose premiums jump dramatically for higher policy limits.

| Insurance Company | $200k Policy | $300k Policy | $500k Policy |

|---|---|---|---|

| $43 | $61 | $81 | |

| $63 | $96 | $142 | |

| $64 | $105 | $149 | |

| $72 | $106 | $138 | |

| $75 | $116 | $139 | |

| $88 | $108 | $166 | |

| $92 | $168 | $213 | |

| $93 | $127 | $210 | |

| $107 | $151 | $213 | |

| $113 | $170 | $231 |

Home insurance rates in North Carolina depend on factors like home value, location, coverage level, and risks from severe weather, with optional add-ons like flood or windstorm coverage for added protection.

A homeowners insurance in NC calculator can help estimate costs based on specific coverage needs and provider rates. With inflation and natural disasters compelling the North Carolina homeowners' insurance rate to be increased, a comparison of insurers is required. Moreover, mortgage lenders require sufficient coverage under North Carolina homeowners insurance laws, which makes increasing policies with increasing property value a necessity.

Comparing Home Insurance Coverage in NC

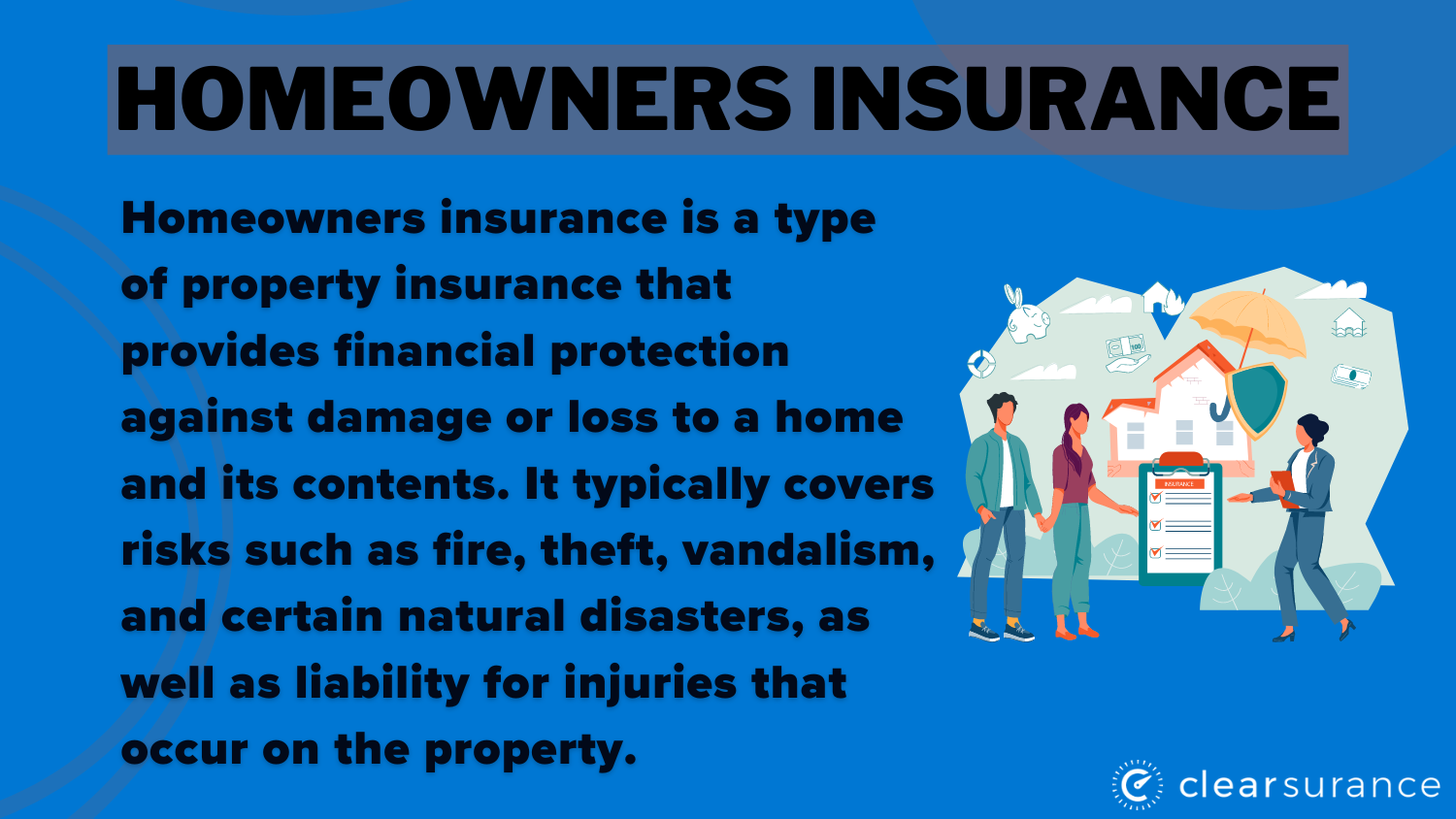

When comparing home insurance in North Carolina, coverage options play a crucial role in determining the best policy for your needs. All standard homeowners insurance policies in North Carolina typically include these fundamental protections:

- Dwelling Coverage: Protects the physical structure of your home against covered perils such as fire, wind, hail, and lightning.

- Personal Property Coverage: Covers your belongings inside the home, including furniture, clothing, electronics, and other personal items if they're damaged or destroyed by a covered event.

- Liability Protection: Provides financial protection if someone is injured on your property and you're found legally responsible. This also covers legal defense costs if you're sued.

- Additional Living Expenses: If your home becomes uninhabitable due to a covered loss, this helps pay for temporary housing, food, and other necessary costs while your home is being repaired.

Our analysis of average homeowners insurance in NC reveals that leading insurers such as Progressive, USAA, and Geico all offer comprehensive protection against water backup, earthquake damage, and identity theft.

While seeking home insurance quotes in North Carolina, it's noteworthy that companies offer various optional endorsements to enhance your protection. These add-ons address specific risks that standard policies may exclude or limit:

| Insurance Company | Water Backup | Earthquake | Identity Theft | Equipment Breakdown | Service Line |

|---|---|---|---|---|---|

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ❌ | ✅ | ❌ | ❌ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ❌ | ✅ | ✅ | ❌ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ | |

| ✅ | ✅ | ✅ | ✅ | ✅ |

The variation in North Carolina home insurance coverage highlights the importance of carefully reviewing policy details, as even major providers like Liberty Mutual, Travelers, and Nationwide maintain identical coverage limitations despite their varying premium rates.

Read More: Homeowners Insurance Claim Check Questions

Saving on Homeowners Insurance in North Carolina

Finding cheap homeowners insurance in North Carolina is easier when taking advantage of discounts like bundling, claims-free history, and loyalty rewards. State Farm leads with the most generous bundling discount at 20%, while Farmers offers the highest claims-free discount at 25%.

| Insurance Company | Bundling | Claims-Free | Home Security | New Home | Loyalty |

|---|---|---|---|---|---|

| 15% | 20% | 10% | 5% | 8% | |

| 10% | 22% | 12% | 6% | 10% | |

| 12% | 25% | 14% | 8% | 7% | |

| 18% | 15% | 8% | 4% | 12% | |

| 14% | 20% | 9% | 5% | 6% | |

| 11% | 18% | 10% | 7% | 9% | |

| 16% | 21% | 11% | 9% | 10% | |

| 20% | 24% | 15% | 6% | 12% | |

| 13% | 16% | 7% | 4% | 8% | |

| 10% | 23% | 12% | 5% | 11% |

How home improvement projects affect your insurance depends on factors like home security upgrades, which can decrease home insurance quotes in NC. Maximizing such discounts can significantly decrease your calculation of your home insurance quotations in NC, so it is worth comparing insurers and maximizing available savings opportunities.

Best Low-Cost Home Insurance in North Carolina

When looking for the best and cheapest home insurance in North Carolina, these firms are always the leading. With the cheapest homeowners insurance in NC at $43 per month for a $200k policy, Progressive stands out with their advanced mobile claims process that settles claims within 15 minutes - an exclusive feature found only on their platform.

USAA, though exclusive to military members, ranks second, offering unmatched military-specific coverage options that other insurers simply don't provide. Geico rounds out the top three best homeowners insurance in North Carolina, setting themselves apart through their extensive smart security system partnerships.

While all these insurers embrace Smart home devices for discounts, each has something special in store. Such special features, with their competitive pricing and full coverage options, make them a highlight among North Carolina homeowners in search of good quality protection at budget-friendly rates. Secure cheap insurance for your home by entering your ZIP code into our free quote comparison tool.

Frequently Asked Questions

What happens if I need to file multiple claims within my first year of coverage?

Filing multiple claims can trigger rate increases up to 15-18% depending on the provider, while consumer homeowners insurance complaints show this is a common concern among first-time policyholders.

How does North Carolina's coastal location affect homeowners insurance rates?

Coastal properties within 50 miles of the shoreline face significantly higher premiums and deductibles due to hurricane risks, with some insurers like Progressive charging up to double the standard rates for these locations.

Secure cheap insurance for your home by entering your ZIP code into our free quote comparison tool.

Are smart home security systems worth investing in for insurance savings?

Yes, smart security installations can yield 10-15% premium reductions, but consider maintenance costs and required internet connectivity for maximum benefits.

What uncommon damages are covered under standard policies?

While basic policies cover common issues, damages ranging from raccoon vandalism to flooding often require additional coverage or specific riders for protection.

How long does it typically take to get coverage approval in North Carolina?

Approval times vary from 24 hours to 2 weeks, with factors like home age, location, and required inspections affecting processing time.

Can I transfer my existing policy discounts to a new insurer?

While claims-free histories typically transfer, loyalty discounts usually don't, requiring a new earning period with the new provider.

What coverage gaps should homeowners be aware of when choosing basic policies?

From home improvement, contractor theft & homeowners insurance coverage to foundation damage, many standard policies exclude these essential protections, requiring additional riders.

What role does credit score play in North Carolina homeowners insurance rates?

Insurance providers use credit-based insurance scores to determine rates, potentially affecting premiums by 20-50%.

How do renovation projects impact existing coverage?

Major renovations may require temporary policy adjustments, with some insurers like Farmers offering specific coverage during construction without premium increases.

What documentation is needed for emergency response team services?

Most insurers require pre-registration for emergency response services, including current photos, home inventory, and emergency contact information.

Make sure your home is protected by entering your ZIP code into our home insurance comparison tool today.